S-1/A: General form of registration statement for all companies including face-amount certificate companies

Published on May 25, 2012

Table of Contents

As filed with the Securities and Exchange Commission on May 25, 2012

Registration No. 333-176767

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

RESTORATION HARDWARE HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 5712 | 45-3052669 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

15 Koch Road, Suite J

Corte Madera, CA 94925

(415) 924-1005

(Address, including zip code, and telephone number, including area code, of registrants principal executive offices)

Gary G. Friedman

Chairman and Co-Chief Executive Officer

Carlos E. Alberini

Co-Chief Executive Officer

15 Koch Road, Suite J

Corte Madera, CA 94925

(415) 924-1005

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Stewart L. McDowell, Esq. Steven R. Shoemate, Esq. Gibson Dunn & Crutcher, LLP 555 Mission Street San Francisco, CA 94105 Tel: (415) 393-8200 Fax: (415) 986-5309 |

Gavin B. Grover, Esq. John M. Rafferty, Esq. Andrew D. Thorpe, Esq. Morrison & Foerster LLP 425 Market Street San Francisco, CA 94105 Tel: (415) 268-7000 Fax: (415) 268-7522 |

Sharon R. Flanagan, Esq. Bradley S. Fenner, Esq. Sidley Austin LLP 555 California Street San Francisco, CA 94104 Tel: (415) 772-1200 Fax: (415) 772-7400 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of large accelerated filer, accelerated filer and smaller reporting company in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee |

||||||

| Class A common stock, $0.0001 par value |

$ | 150,000,000 | (3 | ) | ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes offering price of shares that the underwriters have the option to purchase. |

| (3) | Registration fee for the Class A common stock being offered under this amended Registration Statement has been previously paid at the time of the initial filing of this Registration Statement on September 9, 2011. |

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated May 25, 2012

P R O S P E C T U S

Shares

Class A Common Stock

This is Restoration Hardware Holdings, Inc.s initial public offering.

We are selling shares of our Class A common stock and the selling stockholders identified in this prospectus are selling shares of our Class A common stock. We will not receive any of the proceeds from the sale of shares to be offered by the selling stockholders.

Following this offering, we will have two classes of authorized common stock, Class A common stock and Class B common stock. The rights of the holders of Class A common stock and Class B common stock will be identical, except with respect to voting and conversion. Each share of Class A common stock is entitled to one (1) vote per share. Each share of Class B common stock is entitled to 3.5 votes per share and is convertible into one (1) share of Class A common stock upon the occurrence of certain events. Upon completion of this offering, holders of our Class B common stock will control common stock representing % of the total voting power of our common stock.

We expect the public offering price to be between $ and $ per share of Class A common stock. Prior to this offering, there has been no public market for the Class A common stock. After pricing this offering, we expect that the Class A common stock will trade on the under the symbol RH.

We are an emerging growth company as defined in the Jumpstart Our Business Startups Act of 2012 and, as such, will be subject to reduced public company reporting requirements.

Investing in our Class A common stock involves risks that are described in the Risk Factors section beginning on page 17 of this prospectus.

| Per Share | Total |

|||||

| Public offering price |

$ | $ | ||||

| Underwriting discount |

$ | $ | ||||

| Proceeds, before expenses, to us |

$ | $ | ||||

| Proceeds, before expenses, to the selling stockholders |

$ | $ |

The underwriters may also exercise their option to purchase up to an additional shares of Class A common stock from the selling stockholders, at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares of Class A common stock will be ready for delivery on or about , 2012.

| BofA Merrill Lynch | Goldman, Sachs & Co. |

The date of this prospectus is , 2012.

Table of Contents

| Page | ||||

| ii | ||||

| 1 | ||||

| 17 | ||||

| 39 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

| 45 | ||||

| Selected Historical Consolidated Financial and Operating Data |

47 | |||

| Managements Discussion and Analysis of Financial Condition and Results of Operations |

51 | |||

| 77 | ||||

| 96 | ||||

| 103 | ||||

| 113 | ||||

| 115 | ||||

| 121 | ||||

| 123 | ||||

| 128 | ||||

| Material U.S. Federal Income Tax Considerations to Non-U.S. Holders of our Class A Common Stock |

130 | |||

| 134 | ||||

| 141 | ||||

| 141 | ||||

| 142 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus or in any free writing prospectus that we authorize to be delivered to you. Neither we nor the selling stockholders or underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

i

Table of Contents

We use a 52 53 week fiscal year ending on the Saturday closest to January 31. Fiscal years are identified in this prospectus according to the calendar year prior to the calendar year in which they end. For example, references to 2011, fiscal 2011 or similar references refer to the fiscal year ended January 28, 2012.

All of the outstanding capital stock of Restoration Hardware, Inc. was acquired on June 16, 2008, by Home Holdings, LLC, which we refer to in this prospectus as the Acquisition. Home Holdings equity interests are held primarily by (i) CP Home Holdings, LLC, an investment entity managed by funds affiliated with Catterton Management Company, LLC, (ii) Tower Three Home LLC, an investment fund managed by Tower Three Partners, LLC, and (iii) funds affiliated with Glenhill Capital Management LLC. In this prospectus, we refer to CP Home Holdings, LLC and its affiliated funds as Catterton, we refer to Tower Three Home LLC and its affiliated funds as Tower Three and we refer to Glenhill Capital Management LLC and its affiliated funds as Glenhill. As a result of the Acquisition, a new basis of accounting was created beginning June 17, 2008. In this prospectus, the periods prior to the Acquisition are referred to as the Predecessor periods and the periods after the Acquisition are referred to as the Successor periods. The Predecessor periods presented in this prospectus for 2008 include the period from February 3, 2008 through June 16, 2008, reflecting approximately 19 weeks of operations, and the Successor periods presented in this prospectus for 2008 include the period from June 17, 2008 through January 31, 2009, reflecting approximately 33 weeks of operations. Due to the Acquisition, the financial statements presented in this prospectus for the Successor periods are not comparable to those of the Predecessor periods.

In this prospectus, when we refer to store level cash contribution margin, we mean store net revenues less product costs and cash operating costs related to store operations, divided by store net revenues.

In this prospectus, when we refer to store demand in a market, we mean the dollar value of orders booked by customers associated with that particular location for the specified period.

In this prospectus, when we refer to direct demand in a market, we mean the dollar value of orders booked by customers through catalogs and e-commerce in that market for the specified period.

ii

Table of Contents

This summary highlights some of the key information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider in making your investment decision. You should read the following summary together with the entire prospectus carefully, including Risk Factors, Managements Discussion and Analysis of Financial Condition and Results of Operations, the more detailed information regarding our Company and the common stock being sold in this offering, as well as our consolidated financial statements and the related notes appearing elsewhere in this prospectus, before deciding to invest in our common stock. Some of the statements in this prospectus constitute forward-looking statements. See Forward-Looking Statements and Market Data.

Except where the context otherwise requires or where otherwise indicated, the terms Restoration Hardware, we, us, our, our Company and our business refer, prior to the Reorganization discussed below, to Restoration Hardware, Inc. and, after the Reorganization, to Restoration Hardware Holdings, Inc., in each case together with its consolidated subsidiaries, including Restoration Hardware, Inc., as a combined entity. The term Restoration Hardware Holdings refers to Restoration Hardware Holdings, Inc. and the term Home Holdings refers to Home Holdings, LLC, and, in each case, not to any of their subsidiaries.

Our Company

We believe Restoration Hardware is one of the most innovative and fastest growing luxury brands in the home furnishings marketplace. We believe our brand stands alone and is disrupting and redefining this highly fragmented and growing market, contributing to our superior sales growth and market share gains over the past several years. Our unique ability to innovate, curate and integrate products, categories, services and businesses with a completely authentic and distinctive point of view, then rapidly scale them across our fully integrated multi-channel infrastructure is a powerful platform for continued long-term growth. Additionally, our unique product development, go-to-market and supply chain capabilities, together with our significant scale, enable us to offer a compelling combination of design, quality and value that we believe is unparalleled in the marketplace.

Our business is fully integrated across our multiple channels of distribution, consisting of our stores, catalogs and websites. As of January 28, 2012, we operated a total of 74 retail stores, consisting of 72 Galleries and 2 full line Design Galleries, and 10 outlet stores throughout the United States and Canada. In fiscal 2011, we distributed approximately 26.1 million catalogs, and our websites logged over 14.3 million unique visits.

Over the last several years, we achieved strong growth in sales and profitability, as illustrated by the following:

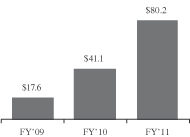

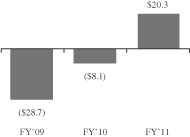

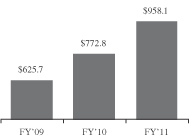

| | From fiscal 2009 to fiscal 2011, we increased our net revenues 53% to $958.1 million, our Adjusted EBITDA 356% to $80.2 million and our Adjusted EBITDA margin by 555 basis points to 8.4%. Over the same time period we increased our net income by $49.0 million from a net loss of $28.7 million to net income of $20.3 million; and |

| | We achieved eight consecutive quarters of double-digit net revenue growth through our fiscal quarter ended January 28, 2012. We achieved this growth as we reduced our store base from 95 retail locations as of January 30, 2010, to 74 locations as of January 28, 2012. |

1

Table of Contents

| Net revenues |

Adjusted EBITDA |

Net income (loss) |

||

| (dollars in millions) | ||||

|

|

|

|

||

See Prospectus SummarySummary Historical Consolidated Financial and Operating Data for a discussion of Adjusted EBITDA and a reconciliation of the differences between Adjusted EBITDA and net income (loss).

Our Competitive Strengths

We attribute our success to the following competitive strengths:

Our Market-Redefining Luxury Brand. We believe Restoration Hardware stands alone as a leading luxury brand of inspired design, and is redefining the highly fragmented home furnishings market by offering a compelling combination of design, quality and value. We believe we are disrupting the home furnishings competitive landscape by attracting affluent consumers from designer showrooms and high-end boutiques, as well as aspirational consumers trading up from department stores and other home furnishings retailers. In a market characterized by smaller, independent competitors, we believe our luxury positioning, superior quality and significant scale enable us to continue to rapidly grow our market share.

Our Unique Development Model. We believe our unique approach to the development of new products, categories and services enables us to gain market share, adapt our business to emerging trends, stay relevant with our customers and enter into new businesses that leverage our strengths. The foundation of our unique development model is:

| | Innovation. We are dedicated to offering products and services that push established boundaries. The scope of our innovation is demonstrated in every aspect of our organization, including in our products and services, our stores and presentation, our channel-agnostic go-to-market strategy and our fully integrated supply chain and systems infrastructure. |

| | Curation. At our core we are not designers, rather we are curators and composers of inspired design and experiences. We travel the world in search of people, ideas, items, experiences and inspiration, and then create a composition that is unique and entirely our own. |

| | Integration. Everything we curate and compose must be beautifully and intelligently integrated, enhancing the appeal of our offering and experience. This process involves both art and science as we integrate new products, categories, services and businesses that enhance our existing offering, and as our supporting functions and infrastructure are integrated to achieve our goals. |

Our ability to innovate, curate and integrate products, categories, services and businesses, then rapidly scale them across our fully integrated multi-channel infrastructure is a powerful platform for continued long-term growth.

Our Superior Capabilities. Our product development and multi-channel go-to-market capabilities, together with our fully integrated infrastructure and significant scale, enable us to offer a compelling combination of design, quality and value that we believe is unparalleled in the marketplace.

2

Table of Contents

| | Highly Differentiated Product Development Capabilities. We have established a cross-functional organization centered on product leadership, with teams that collaborate across functions and work closely with our network of artisan partners. Our product development platform and significant scale have enabled us to introduce an increasing number of new products with each collection and dramatically shorten our product lead times, while allowing us to offer greater value to our customers. |

| | Multi-Channel Go-To-Market Ability. We pursue a market-based rather than a channel-based sales strategy where we size our stores to the potential of the area that each location serves and leverage our direct channels to provide access to our complete product offering. This approach is designed to enhance the customer experience, generate greater sales, increase our market share and deliver higher returns on invested capital. |

| | Fully Integrated Infrastructure. Our infrastructure is integrated across our channels, providing strong direct sourcing capabilities, a centrally managed inventory and a reconfigured distribution network and new order management, warehouse management and point-of-sale systems. We believe our sophisticated operating platform provides us with significant capabilities to support our future growth. |

Our High-Performance Culture and Team. We have built a high-performance organization driven by a company-wide commitment to our core values of People, Quality, Service and Innovation. We believe our leadership team, led by our Co-Chief Executive Officers, Gary Friedman and Carlos Alberini, is a key driver of our success and positions us to execute our long-term growth strategy.

Our Growth Strategy

Key elements of our growth strategy are to:

Transform Our Real Estate Platform. We believe we have an opportunity to significantly increase our sales by transforming our real estate platform from a mall-based retail footprint to a portfolio focused on full line Design Galleries. With a target size of approximately 21,500 square feet of selling space, our full line Design Galleries have approximately three times the selling square footage of our current average Gallery. We have identified approximately 50 key metropolitan markets where we can open new full line Design Galleries. We believe that we have the opportunity to double our current selling square footage in the U.S. and Canada over the next 7 to 10 years.

In 2011, we opened our first two full line Design Galleries in Los Angeles and Houston where we consolidated demand by closing existing retail stores in each market. In the Los Angeles market, we have increased store demand by 85% and direct demand by 30% and in the Houston market, we have increased store demand by over 60% and direct demand by over 50%, in each case from the date of opening our new full line Design Gallery in that market to May 19, 2012. Over the next 24 months, we plan to open full line Design Galleries in iconic or high profile locations in Scottsdale, Boston, Greenwich (Connecticut) and Atlanta. We are also actively exploring opening Design Galleries in other key markets such as New York City, Miami, Dallas and Chicago.

Expand Our Offering and Increase Our Market Share. We participate in the domestic housewares and home furnishings market, that based on our research we believe represented $143 billion in sales in 2010. Our annual net revenues currently represent less than 1% of this market, and we believe we have a significant opportunity to increase our market share by:

| | Growing our merchandise assortment and introducing new products and categories, including current initiatives in furniture, rugs, lighting, tabletop and baby and child; |

| | Expanding our service offerings including interior design, product customization and gift registry services; and |

3

Table of Contents

| | Exploring and testing new business opportunities such as Art & Culture and Hospitality that leverage our defining strengths of taste, style and innovation. |

Increase Brand Awareness. We will continue to increase our brand awareness and customer loyalty through our real estate transformation, our circulation strategy, our digital and social media marketing initiative, and our increased advertising and public relations efforts. Our stores are a critical branding vehicle and we believe the transformation of our real estate platform to a portfolio focused on full line Design Galleries will contribute to increased brand awareness as our customers experience an enhanced expression of our luxury brand positioning. Our catalogs are also an important branding and advertising vehicle. Our Source Book strategy has contributed to a 41% increase in the number of catalog pages circulated and a 27% increase in net revenues for our direct business in fiscal 2011. We are planning to increase the number of catalog pages circulated in fiscal 2012 by more than 30%.

Pursue International Expansion. We plan to strategically expand our business into select countries outside of the United States and Canada over the next several years. We believe that our luxury brand positioning and unique aesthetic will have strong international appeal.

Increase Operating Margins. We have the opportunity to continue to improve our operating margins by leveraging our fixed occupancy costs and scalable infrastructure, and by expanding our merchandise margins. We believe that our real estate transformation, specifically consolidating multiple Galleries into single full line Design Galleries, will allow us to better leverage our fixed occupancy costs.

For a discussion of risks that could adversely affect our growth strategies, see Risk FactorsRisks Related to Our Business.

Our High-Performance Culture

Our culture is driven by our management team, which instills a company-wide commitment to our core values of People, Quality, Service and Innovation. We believe our distinct corporate culture allows us to attract highly talented team members who are passionate and driven and who share our vision.

Evolution of Our Business

When Gary Friedman joined us as Chief Executive Officer in 2001, we began to reposition Restoration Hardware from a nostalgic, discovery-items business to a leading home furnishings brand. In 2008, we were taken private by investment funds affiliated with Catterton, Tower Three and Glenhill. As a private company, we were able to accelerate the pace of the transformation of our business and brand and the development of our multi-channel business model and infrastructure. Over the last eleven years, we built a new company as we:

| | Elevated our brand positioning; |

| | Enhanced our product development process; |

| | Refined our go-to-market strategy; |

| | Reconceptualized our stores and developed our full line Design Gallery format; |

| | Built a new supply chain and systems infrastructure; and |

| | Strengthened our management team. |

We believe these initiatives have contributed to our recent strong performance and increased profitability, and position us for sustained growth and profitability.

Our Market

We participate in the large and growing domestic housewares and home furnishings market. Based on our research, we believe this market generated $143 billion in retail sales in 2010 and is projected to grow at a

4

Table of Contents

compound annual growth rate of 3% 4% between 2011 and 2015. Our net revenues currently represent less than 1% of this market, providing us with a substantial opportunity to gain market share.

According to Euromonitor International, a market research and analysis firm, the housewares and home furnishings market is highly fragmented. The top 20 companies comprised only 20% of the total market in 2008, with the largest player representing less than 3% of the total market. As a result of the weakening housing market and economic downturn in 2007, many home furnishings retailers were forced to close stores, dramatically scale back operations or lower prices. While our sales results were also adversely affected during this period, this disruption also created an opportunity for us to differentiate our brand in the marketplace. We believe we are well positioned to gain market share in the current competitive environment as a result of our compelling combination of design, quality and value.

We target households with incomes of $200,000 and higher, which we believe drive a disproportionate share of spending in the home furnishings market. We believe that these consumers are highly attractive as they tend to be less impacted by an economic downturn and return to spending more quickly in an economic recovery.

Summary Risk Factors

We are subject to a number of risks, including risks that may prevent us from achieving our business objectives or that may adversely affect our business, financial condition, results of operations, cash flows and prospects. You should carefully consider the following risks, including the risks discussed in the section entitled Risk Factors, before investing in our common stock:

| | We are undertaking a large number of business initiatives at the same time and if these new initiatives are not successful, they may have a negative impact on our operating results. |

| | Growth in our business may not be sustained and may not generate a corresponding improvement in our results of operations. |

| | If we fail to successfully anticipate consumer preferences and demand, or to manage our inventory commensurate with demand, our results of operations may be adversely affected. |

| | Our growth strategy and performance depend on our ability to purchase our merchandise in sufficient quantities at competitive prices, including our products that are produced by artisans and specialty vendors, and any disruptions we experience in our ability to obtain our products in a timely fashion or in the quantities required could have a material adverse effect on our business. |

| | If any of our vendors is not able to meet our product requirements, we may not be able to develop relationships with new alternative vendors to replace those product requirements in a timely and satisfactory manner, which could lead to product shortages and customer backorders, which could harm our business. |

| | We do not have exclusive relationships with many of our vendors, and there is a risk that our vendors may sell similar or identical products to our competitors, which could harm our business. |

| | We may not have adequate remedies with our vendors for defective merchandise, which could damage our reputation and brand image and harm our business. |

| | Changes in consumer spending or the housing market may significantly harm our revenue and results of operations. |

| | If we lose key personnel or are unable to hire additional qualified personnel, our business may be harmed. |

| | Our operations have significant liquidity and capital requirements and depend on the availability of adequate financing on reasonable terms, and if we are unable to borrow sufficient capital, it could have a significant negative effect on our business. |

5

Table of Contents

| | A number of factors that affect our ability to successfully open new stores or to optimize our store footprint are beyond our control, and these factors may harm our ability to execute our strategy of sizing stores to the potential of the market, which may negatively affect our results of operations. |

| | Our operating results are subject to quarterly and seasonal fluctuations, and results for any quarter may not necessarily be indicative of the results that may be achieved for the full fiscal year. |

| | Our business depends in part on a strong brand image. We continue to invest in the development of our brand and the marketing of our business, and if we are not able to maintain and enhance our brand or market our product offerings, we may be unable to attract a sufficient number of customers or sell sufficient quantities of our products. |

| | We are exploring opportunities to expand into new categories or complementary businesses. If we are not successful in these new categories or business areas, it may have an adverse effect on our results of operations and our reputation. |

| | Voting control of our common stock is concentrated in certain stockholders who held our stock prior to this offering, including Home Holdings and our Co-Chief Executive Officers. The dual-class structure of our common stock has the effect of increasing the amount of voting control held by our Co-Chief Executive Officers. This concentration of voting control will limit your ability to influence corporate matters. |

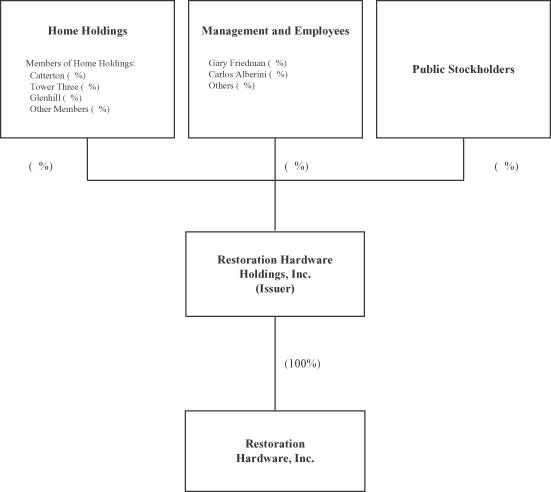

Reorganization

Restoration Hardware Holdings was incorporated as a Delaware corporation on August 18, 2011, by our sole stockholder, Home Holdings, for the purpose of acquiring all of the stock of Home Holdings wholly owned subsidiary, Restoration Hardware, Inc. Restoration Hardware Holdings will acquire all of the outstanding shares of Restoration Hardware, Inc. prior to the effectiveness of this offering. Outstanding units under the 2008 Home Holdings equity compensation plan, which we refer to as the Team Resto Ownership Plan, will be converted in connection with this offering into restricted and unrestricted Class A common stock, or, in the case of units owned by Mr. Friedman or Mr. Alberini, Class B common stock, and the vesting status of the Home Holdings units will carry over to our Class A common stock, or, in the case of Mr. Friedman or Mr. Alberini, Class B common stock, with unvested shares constituting restricted stock of the applicable class. In this prospectus, we refer to these transactions as the Reorganization.

Principal Equity Holders

Home Holdings equity interests are held primarily by funds affiliated with Catterton, Tower Three and Glenhill. In this prospectus, we refer to Catterton, Tower Three and Glenhill as our Principal Equity Holders.

Home Holdings will remain in place after the completion of this offering and will continue to be the single largest holder of our common stock. Interests of Catterton, Tower Three and Glenhill in our Company will continue to be held indirectly through their ownership interests in Home Holdings.

Catterton. Catterton is a leading private equity firm with an exclusive focus on providing equity capital in support of small to middle-market consumer companies that are positioned for attractive growth. Since its founding in 1989, Catterton has invested in approximately 80 companies and led equity investments totaling over $3.3 billion. Presently, Catterton is actively managing more than $2.5 billion of equity capital focused on all sectors of the consumer industry: food, beverage, retail, restaurants, consumer products, consumer services and media and marketing services. Cattertons combination of investment capital, strategic operating skills and industry network has enabled it to become a highly sought after firm within this industry.

6

Table of Contents

Tower Three. Tower Three is an operationally-focused private equity fund formed to create a concentrated portfolio of investments in U.S.-based middle-market businesses. Tower Threes professionals are experienced with operational management, financial restructuring, private equity and credit markets. With long-term committed capital from major institutional investors, Tower Three has the flexibility to participate in a variety of transactions.

Glenhill. Glenhill is a privately owned investment partnership that invests primarily in public equity markets internationally. Founded in 2001, Glenhill is led by Glenn J. Krevlin, who has served as the managing member of Krevlin Advisors, LLC, an investment management firm, which is the general partner of Glenhill.

Funds affiliated with Catterton and Tower Three invested in Home Holdings in order to fund Home Holdings acquisition of Restoration Hardware, Inc. Funds associated with Glenhill acquired their interests in Home Holdings pursuant to a rollover agreement, pursuant to which such funds agreed to contribute a portion of their shares of Restoration Hardware, Inc.s common stock in exchange for a pro rata equity interest in Home Holdings. See Certain Relationships and Related Party Transactions.

Our Principal Equity Holders are also in the business of making investments in companies and may from time to time acquire and hold interests in businesses that compete directly or indirectly with us. Our Principal Equity Holders may also pursue acquisition opportunities that are complementary to our business and, as a result, those acquisition opportunities may not be available to us. See Risk FactorsOur largest stockholders, including Home Holdings, Catterton, Tower Three, Glenhill, Gary Friedman and Carlos Alberini, will continue to have significant influence over us after this offering, including control over decisions that require the approval of stockholders, and their interests in our business may be different from yours.

Following this offering, we will have two classes of authorized common stock, Class A common stock and Class B common stock. Each share of Class A common stock will be entitled to one (1) vote per share and each share of Class B common stock will be entitled to 3.5 votes per share. Outstanding shares of Class B common stock will represent approximately % of the voting power of our outstanding capital stock following this offering. Gary Friedman and Carlos Alberini, our Co-Chief Executive Officers, will hold all of the outstanding shares of Class B common stock.

7

Table of Contents

The following chart sets forth the anticipated distribution of voting power among our stockholders as of the completion of this offering, assuming no exercise by the underwriters of their option to purchase additional shares of Class A common stock:

Payments to Principal Equity Holders and Officers and Directors in Connection with the Offering

In connection with this offering, pursuant to our management services agreement with affiliates of our Principal Equity Holders, we plan to pay Catterton Management Company, LLC, Tower Three Partners LLC and GJK Capital Advisors, LLC, fees in the amount of $ , $ and $ , respectively. In addition, a portion of the units in Home Holdings held by certain of our officers will vest in connection with this offering, including units held by Gary Friedman, our Chairman and Co-Chief Executive Officer; units held by Carlos Alberini, our Co-Chief Executive Officer; and units held by Ken Dunaj, our Chief Operating Officer. See Executive CompensationEmployee Benefit and Stock PlansTeam Resto Ownership Plan.

8

Table of Contents

Corporate and Other Information

Restoration Hardware Holdings, Inc. is a Delaware corporation. Our corporate headquarters is located at 15 Koch Road, Suite J, Corte Madera, CA 94925. Our telephone number is (415) 924-1005. Our principal website address is www.restorationhardware.com. We also operate a website for our Baby & Child brand at www.rhbabyandchild.com. The information on any of our websites is not deemed to be incorporated in this prospectus or to be part of this prospectus.

This prospectus includes our trademarks, such as Restoration Hardware and Restoration Hardware Baby & Child, which are protected under applicable intellectual property laws and are the property of Restoration Hardware. This prospectus also contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks and trade names.

9

Table of Contents

The Offering

| Total Class A common stock offered |

shares |

| Class A common stock offered by us |

shares |

| Class A common stock offered by the selling stockholders |

shares |

| Class A common stock to be outstanding immediately after this offering |

shares |

| Class B common stock to be outstanding immediately after this offering |

shares |

| Total Class A and Class B common stock to be outstanding immediately after this offering |

shares |

| Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting the underwriting discount and estimated offering expenses, will be approximately $ million, assuming the shares of Class A common stock are offered at $ per share (the midpoint of the estimated price range set forth on the cover of this prospectus). |

| We will not receive any proceeds from the sale of shares of Class A common stock by the selling stockholders. |

| We intend to use the net proceeds from the sale of Class A common stock by us in this offering to repay a portion of the outstanding amounts under the Restoration Hardware, Inc. revolving line of credit and term loan, for general corporate purposes, including working capital and capital expenditures, and to pay other fees and expenses incurred in connection with this offering, including payments to Catterton, Tower Three and Glenhill pursuant to the terms of the management services agreement we have entered into with them. See Use of Proceeds. |

| Voting rights |

After the completion of this offering, our common stock will consist of two classes: Class A common stock and Class B common stock. Purchasers in this offering will acquire Class A common stock. Class A and Class B common stock are identical in all respects, except with respect to voting and conversion rights. Holders of Class A common stock are entitled to one (1) vote per share, and holders of Class B common stock are entitled to 3.5 votes per share, on all matters to be voted on by our common stockholders. Shares of Class A and Class B common stock vote together as a single class on all matters submitted to a vote of stockholders, unless required by law. |

| All of the Class B common stock will be beneficially owned by Gary Friedman and Carlos Alberini, our Co-Chief Executive Officers. Immediately following the completion of this offering, Mr. Friedman |

10

Table of Contents

| will control % of our Class B common stock, representing % of the total voting power of our outstanding common stock, and Mr. Alberini will control % of our Class B common stock, representing % of the total voting power of our outstanding common stock. Mr. Friedman and Mr. Alberini will also have options to purchase Class A common stock. |

| Class B common stock conversion |

Shares of Class B common stock may only be held by Mr. Friedman, Mr. Alberini, or certain of their related parties. Each share of Class B common stock is convertible at any time at the option of the holder into one share of Class A common stock. Shares of Class B common stock that are transferred to a holder other than Mr. Friedman, Mr. Alberini or any of their permitted related parties will automatically convert into a like number of shares of Class A common stock. All of the Class B common stock owned by Mr. Friedman and any of his permitted related parties will convert into Class A common stock on a one-for-one basis on the date upon which Mr. Friedman, and such related parties, beneficially own, in the aggregate, fewer than shares of Class B common stock. All of the Class B common stock owned by Mr. Alberini and any of his permitted related parties will convert into Class A common stock on a one-for-one basis on the date upon which Mr. Alberini, and such related parties, beneficially own, in the aggregate, fewer than shares of Class B common stock. All of the Class B common stock owned by Mr. Friedman or Mr. Alberini or their related parties will also convert into Class A common stock on a one-for-one basis in connection with certain events involving the death, permanent mental disability or termination of employment of Mr. Friedman or Mr. Alberini, as the case may be. See Description of Capital StockClass A Common Stock and Class B Common Stock. |

| Principal stockholders |

Upon completion of this offering, Home Holdings will own shares, or %, of our outstanding Class A common stock, representing % of the total voting power of our outstanding common stock. Of that amount, Catterton will beneficially own shares, or %, of our outstanding Class A common stock, representing % of the total voting power of our outstanding common stock, Tower Three will beneficially own shares, or %, of our outstanding Class A common stock, representing % of the total voting power of our outstanding common stock and Glenhill will beneficially own shares, or %, of our outstanding Class A common stock, representing % of the total voting power of our outstanding common stock. In addition, Mr. Friedman will beneficially own shares, or %, of our Class A common stock and shares, or %, of our Class B common stock, and Mr. Alberini will beneficially own shares, or %, of our Class A common stock and shares, or %, of our Class B common stock. |

| We are a controlled company within the meaning of the listing rules, and therefore will be exempt from certain of the corporate |

11

Table of Contents

| governance listing requirements of the . See ManagementCorporate Governance. |

| Dividend policy |

We currently intend to retain all available funds and any future earnings for use in the operation of our business, and therefore we do not anticipate paying any cash dividends in the foreseeable future. Any future determination to pay dividends will be at the discretion of our board of directors and will depend upon our results of operations, financial condition, capital requirements and other factors that our board of directors deems relevant. We are a holding company, and substantially all of our operations are carried out by our subsidiary, Restoration Hardware, Inc., and its subsidiaries. Restoration Hardware, Inc.s ability to pay dividends to us is limited by the terms of its credit agreement, which may in turn limit our ability to pay dividends on our common stock. Our ability to pay dividends may also be restricted by the terms of any future credit agreement or any future debt or preferred securities of ours or of our subsidiaries. See Dividend Policy. |

| Conflicts of interest |

As described under Use of Proceeds, Bank of America, N.A., an affiliate of Merrill Lynch, Pierce, Fenner & Smith Incorporated, an underwriter in this offering, is a lender under the Restoration Hardware, Inc. revolving line of credit and term loan and may receive more than five percent of the net proceeds of this offering. Thus, Merrill Lynch, Pierce, Fenner & Smith Incorporated may be deemed to have a conflict of interest under the applicable provisions of Rule 5121 of the Conduct Rules of the Financial Industry Regulatory Authority, Inc., or FINRA. Accordingly, this offering will be made in compliance with the applicable provisions of Rules 5110 and 5121 of the Conduct Rules regarding the underwriting of securities of a company with a member that has a conflict of interest within the meaning of those rules. Goldman, Sachs & Co. has agreed to serve as a qualified independent underwriter as defined by FINRA and performed due diligence investigations and reviewed and participated in the preparation of the registration statement of which this prospectus forms a part. No underwriter with a conflict of interest will execute sales in discretionary accounts without the prior written specific approval of the customers. See UnderwritingConflicts of Interest. |

| Risk factors |

Investing in our Class A common stock involves a high degree of risk. See Risk Factors beginning on page 17 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our Class A common stock. |

| Proposed symbol for trading on |

RH |

Unless otherwise indicated, all information in this prospectus relating to the number of shares of our common stock to be outstanding immediately after this offering:

| | excludes unvested restricted shares of our Class A common stock and unvested restricted shares of our Class B common stock that will be issued to our executive officers and other |

12

Table of Contents

| employees and consultants under the Restoration Hardware 2012 Equity Replacement Plan, which we refer to as the Replacement Plan, as replacement grants for awards previously issued pursuant to the Team Resto Ownership Plan; |

| | excludes options to purchase shares of our Class A common stock, each with an exercise price equal to the initial public offering price, that we expect to grant in connection with this offering under the Restoration Hardware 2012 Stock Incentive Plan, which we refer to as the 2012 Plan; |

| | excludes options to purchase shares and shares of our Class A common stock, each with an exercise price equal to $ per share, that we expect to grant in connection with this offering to our Co-Chief Executive Officers, Gary Friedman and Carlos Alberini, respectively, under the 2012 Plan; |

| | excludes additional shares of Class A common stock reserved for future grants under the 2012 Plan; |

| | assumes an initial public offering price of $ per share of Class A common stock (the midpoint of the estimated price range set forth on the cover of this prospectus); and |

| | assumes no exercise by the underwriters of their option to purchase up to additional shares of Class A common stock from the selling stockholders. |

Summary Historical Consolidated Financial and Operating Data

The following tables present Restoration Hardware, Inc.s summary historical consolidated financial and operating data as of the dates and for the periods indicated. Restoration Hardware Holdings was formed as a Delaware corporation on August 18, 2011. Restoration Hardware Holdings will acquire all of the outstanding shares of capital stock of Restoration Hardware, Inc. prior to the effectiveness of this offering in connection with the Reorganization, and will therefore control Restoration Hardware, Inc. Restoration Hardware Holdings has not engaged in any business or other activities except in connection with its formation and the Reorganization. Accordingly, all financial and other information herein relating to periods prior to the completion of the Reorganization is that of Restoration Hardware, Inc.

All of the outstanding capital stock of Restoration Hardware, Inc. was acquired on June 16, 2008, by Home Holdings, which we refer to in this prospectus as the Acquisition.

The summary consolidated financial data for the fiscal years ended January 30, 2010, January 29, 2011, and January 28, 2012 and as of January 28, 2012, were derived from Restoration Hardware, Inc.s consolidated financial statements included elsewhere in this prospectus.

The unaudited financial information for the twelve months ended April 30, 2011, has been derived by adding our financial information for the year ended January 29, 2011, to the financial information for the three months ended April 30, 2011, and subtracting the financial information for the three months ended May 1, 2010. The unaudited financial information for the twelve months ended April 28, 2012, has been derived by adding our financial information for the year ended January 28, 2012, to the financial information for the three months ended April 28, 2012, and subtracting the financial information for the three months ended April 30, 2011. We believe that presentation of unaudited financial information for these twelve-month periods is useful to investors because it presents information about how our business has performed in the twelve-month period immediately preceding the date of our most recent interim financial statements, which allows investors to review our current performance trends over a full year period, and because it presents results for four consecutive quarters, which presentation compensates for seasonal factors that might influence results in a particular quarter within the year.

Restoration Hardware, Inc.s historical results are not necessarily indicative of future operating results. The summary historical consolidated data presented below should be read in conjunction with the sections entitled Risk Factors, Selected Historical Consolidated Financial and Operating Data and Managements Discussion

13

Table of Contents

and Analysis of Financial Condition and Results of Operations and the consolidated financial statements and the related notes thereto and other financial data included elsewhere in this prospectus.

| Year Ended | Last Twelve Months Ended (1) | |||||||||||||||||||

| January 30, 2010 |

January 29, 2011 |

January 28, 2012 |

April 30, 2011 |

April 28, 2012 |

||||||||||||||||

| (dollars in thousands, excluding per share and per square foot data) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Net revenues |

$ | 625,685 | $ | 772,752 | $ | 958,084 | $ | 825,004 | $ | |||||||||||

| Cost of goods sold |

412,629 | 501,132 | 601,735 | 532,275 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

213,056 | 271,620 | 356,349 | 292,729 | ||||||||||||||||

| Selling, general and administrative expenses |

238,889 | 275,859 | 329,753 | 287,219 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations |

(25,833 | ) | (4,239 | ) | 26,596 | 5,510 | ||||||||||||||

| Interest expense |

(3,241 | ) | (3,150 | ) | (5,134 | ) | (3,192 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

(29,074 | ) | (7,389 | ) | 21,462 | 2,318 | ||||||||||||||

| Income tax expense (benefit) |

(423 | ) | 685 | 1,121 | 521 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | (28,651 | ) | $ | (8,074 | ) | $ | 20,341 | $ | 1,797 | $ | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic and diluted net income (loss) per share |

$ | (286,510 | ) | $ | (80,740 | ) | $ | 203,410 | $ | 17,970 | $ | |||||||||

| Basic and diluted average number of shares outstanding |

100 | 100 | 100 | 100 | ||||||||||||||||

| Pro forma net income (loss) per share (2): |

||||||||||||||||||||

| Basic |

$ | |||||||||||||||||||

| Diluted |

$ | |||||||||||||||||||

| Pro forma average number of shares outstanding (2): |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Diluted |

||||||||||||||||||||

| Other Financial and Operating Data: |

||||||||||||||||||||

| Growth in net revenues: |

||||||||||||||||||||

| Stores (3) |

(6 | )% | 15 | % | 22 | % | 17 | % | % | |||||||||||

| Direct |

(15 | )% | 37 | % | 27 | % | 45 | % | % | |||||||||||

| Total |

(10 | )% | 24 | % | 24 | % | 28 | % | % | |||||||||||

| Retail (4): |

||||||||||||||||||||

| Comparable store sales change (5) |

(7 | )% | 19 | % | 25 | % | 19 | % | % | |||||||||||

| Retail stores open at end of period |

95 | 91 | 74 | 89 | ||||||||||||||||

| Average gross square footage (in thousands) (6) |

1,042 | 1,014 | 913 | 999 | ||||||||||||||||

| Average selling square footage (in thousands) (6) |

660 | 641 | 580 | 634 | ||||||||||||||||

| Retail sales per selling square foot (7) |

$ | 525 | $ | 635 | $ | 846 | $ | 668 | $ | |||||||||||

| Direct: |

||||||||||||||||||||

| Catalogs circulated (in thousands) (8) |

31,336 | 46,507 | 26,052 | 44,735 | ||||||||||||||||

| Catalog pages circulated (in millions) (8) |

4,418 | 6,260 | 8,848 | 6,690 | ||||||||||||||||

| Direct as a percentage of net revenues (9) |

39 | % | 43 | % | 44 | % | 44 | % | % | |||||||||||

| Capital expenditures |

$ | 2,024 | $ | 39,907 | $ | 25,593 | $ | 40,986 | $ | |||||||||||

| Adjusted EBITDA (10) |

$ | 17,596 | $ | 41,097 | $ | 80,154 | $ | 52,228 | $ | |||||||||||

14

Table of Contents

| As of January 28, 2012 | ||||||||

| Actual | Pro Forma As Adjusted (11) |

|||||||

| (in thousands) | ||||||||

| Balance Sheet Data: |

||||||||

| Cash and cash equivalents |

$ | 8,511 | $ | |||||

| Working capital (excluding cash and cash equivalents) (12) |

156,505 | |||||||

| Total assets |

586,809 | |||||||

| Revolving line of credit |

107,502 | |||||||

| Term loan |

14,798 | |||||||

| Total debt (including current portion) (13) |

131,040 | |||||||

| Total stockholders equity |

250,462 | |||||||

| (1) | The unaudited financial information for the twelve months ended April 30, 2011, has been derived by adding our financial information for the year ended January 29, 2011, to the financial information for the three months ended April 30, 2011, and subtracting the financial information for the three months ended May 1, 2010. The unaudited financial information for the twelve months ended April 28, 2012, has been derived by adding our financial information for the year ended January 28, 2012, to the financial information for the three months ended April 28, 2012, and subtracting the financial information for the three months ended April 30, 2011. |

| (2) | Pro forma net income (loss) per share gives effect to (i) the Reorganization, (ii) the issuance of shares of Class A common stock in this offering and (iii) the application of a portion of the estimated net proceeds from the sale of Class A common stock by us in this offering to repay a portion of the outstanding amounts under Restoration Hardware, Inc.s revolving line of credit and term loan as if the offering and those transactions had occurred on January 30, 2011. This assumes net proceeds of this offering of $ million, assuming the shares of Class A common stock are offered at $ per share, the midpoint of the estimated price range set forth on the cover of this prospectus, after deducting the underwriting discount and estimated offering expenses. |

| (3) | Store data represent retail stores plus outlet stores. |

| (4) | Retail data have been calculated based upon retail stores, including our Baby & Child stores, and exclude outlet stores. |

| (5) | Comparable store sales have been calculated based upon retail stores that were open at least fourteen full months as of the end of the reporting period and did not change square footage by more than 20% between periods. Comparable store sales exclude revenues from outlet stores. |

| (6) | Average square footage (gross or selling, as applicable) is calculated for each quarter by taking the total applicable square footage at the beginning of the quarter plus the total applicable square footage at the end of the quarter and dividing by two. Average square footage for periods of six, nine and twelve months is calculated by averaging the average square footage for the quarters within such periods. |

| (7) | Retail sales per selling square foot is calculated by dividing total net revenues for all retail stores, comparable and non-comparable, by the average selling square footage for the period. |

| (8) | The catalogs and catalog pages circulated from period to period do not take into account different page sizes per catalog distributed. Page sizes and page counts vary for different catalog mailings and we sometimes mail different versions of a catalog at the same time. Accordingly, period to period comparisons of catalogs circulated and catalog pages circulated do not take these variations into account. In fiscal 2010, we mailed a larger number of catalogs that contained fewer pages and in some cases significantly smaller page sizes than in prior periods. In fiscal 2011, we mailed fewer catalogs that contained a significant increase in number of pages as compared to fiscal 2010. |

| (9) | Direct revenues include sales through our catalogs and websites. |

| (10) | A reconciliation of net income (loss) under accounting principles generally accepted in the United States (GAAP) to EBITDA and Adjusted EBITDA is set forth below in Selected Historical Consolidated Financial and Operating Data. |

| EBITDA and Adjusted EBITDA have been presented in this prospectus and are supplemental measures of financial performance that are not required by, or presented in accordance with, GAAP. EBITDA is defined as consolidated net income (loss) before depreciation and amortization, interest expense and |

15

Table of Contents

| provision for income taxes. Adjusted EBITDA is calculated in accordance with and is the basis of our Management Incentive Program (or MIP), which is our cash-based incentive compensation program designed to motivate and reward annual performance for eligible employees, and reflects further adjustments to EBITDA to eliminate the impact of certain items, including non-cash or other items that we do not consider representative of our ongoing operating performance, as discussed in more detail in the section entitled Selected Historical Consolidated Financial and Operating Data. |

| EBITDA and Adjusted EBITDA are included in this prospectus because they are key metrics used by management, our board of directors and our Principal Equity Holders to assess our financial performance, and Adjusted EBITDA is used in connection with determining incentive compensation under our MIP. Additionally, EBITDA is frequently used by analysts, investors and other interested parties to evaluate companies in our industry. We use Adjusted EBITDA, alongside other GAAP measures such as gross profit, operating income (loss) and net income (loss), to measure profitability, to make budgeting decisions, and to compare our performance against that of other peer companies. We believe that Adjusted EBITDA provides useful information facilitating operating performance comparisons from period to period and company to company. |

| EBITDA and Adjusted EBITDA are not GAAP measures of our financial performance or liquidity and should not be considered as alternatives to net income (loss) as a measure of financial performance, cash flows from operating activities as a measure of liquidity or any other performance measure derived in accordance with GAAP, and they should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Additionally, EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow for managements discretionary use, as they do not consider certain cash requirements such as tax payments and debt service requirements and certain other cash costs that may recur in the future. EBITDA and Adjusted EBITDA contain certain other limitations, including the failure to reflect our cash expenditures, cash requirements for working capital needs and cash costs to replace assets being depreciated and amortized, and exclude certain unusual charges that may recur in the future. In evaluating Adjusted EBITDA, you should be aware that in the future we may incur expenses that are the same as or similar to some of the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed to imply that our future results will be unaffected by any such adjustments. Management compensates for these limitations by relying primarily on our GAAP results and by using EBITDA and Adjusted EBITDA only supplementally. Our measures of EBITDA and Adjusted EBITDA are not necessarily comparable to other similarly titled captions of other companies due to different methods of calculation. |

| (11) | Pro Forma as Adjusted amounts give effect to (i) the Reorganization, (ii) the issuance of shares of Class A common stock in this offering, (iii) the application of $ million of estimated net proceeds of this offering to repay a portion of the outstanding amounts under the revolving line of credit and term loan, (iv) the use of $ million of the estimated net proceeds to pay other fees and expenses incurred in connection with this offering, including management fees of $ to Catterton, Tower Three and Glenhill pursuant to the terms of the management services agreement with them, (v) $ non-cash impact to accumulated deficit for stock based compensation charges related to the shares of restricted stock that become vested upon this offering, and (vi) additional cash payments of $2.2 million to former employees that are due as a result of this stock offering. A $1.00 increase (decrease) in the assumed initial public offering price of $ per share of Class A common stock, the midpoint of the estimated price range set forth on the cover of this prospectus, would increase (decrease) the pro forma as adjusted amount of cash and cash equivalents by $ million, total assets by $ million, revolving line of credit by $ million, total debt (including current portion) by $ million and total stockholders equity by $ million, assuming the number of shares of Class A common stock offered by us, as set forth on the cover of this prospectus, remains the same and after deducting the underwriting discount and estimated offering expenses. |

| (12) | Working capital is defined as current assets, excluding cash and cash equivalents, less current liabilities, excluding the current portion of long-term debt. |

| (13) | Total debt (including current portion) includes amounts outstanding under the revolving line of credit, term loan and capital lease obligations. |

16

Table of Contents

This offering and an investment in our Class A common stock involve a high degree of risk. You should carefully consider the risks and uncertainties described below, together with the risks and uncertainties described elsewhere in this prospectus, including our consolidated financial statements and the related notes contained elsewhere in this prospectus, before you decide to purchase shares of our Class A common stock. If any of the following risks or uncertainties actually occurs, our business, financial condition, results of operations, cash flow and prospects could be materially and adversely affected. As a result, the price of our Class A common stock could decline and you could lose all or part of your investment in our Class A common stock.

Risks Related to Our Business

We are undertaking a large number of business initiatives at the same time and if these new initiatives are not successful, they may have a negative impact on our operating results.

We are in the process of an ongoing major transformation of our business characterized by a period of rapid growth and a large number of new business initiatives. For example, we recently developed a full line Design Gallery format which involves larger store square footage. We plan to continue to open full line Design Galleries in select major metropolitan markets and we expect to close a number of our older stores and replace them with the full line Design Gallery format. We are currently contemplating other new product lines and extensions, as well as expanding sales to international markets. In addition, we are continuing a number of new initiatives in other areas of our business, including product sourcing and distribution and management information systems. For example, we have reduced the use of third-party buying agents in most foreign locations. In addition, we have significantly expanded the page counts of our catalogs, increased the number of households receiving our catalogs and reduced the number of catalog mailings.

The number of current business initiatives could strain our financial, operational and management resources. In addition, these initiatives may not be successful. If we are not successful in managing our current growth and the large number of new initiatives that are underway, we might experience an adverse impact on our financial performance and results of operations. All of the foregoing risks may be compounded in any economic downturn. In addition, if we fail to achieve the intended results of our current business initiatives, or if the implementation of these initiatives is delayed or abandoned, diverts managements attention or resources from other aspects of our business or costs more than anticipated, we may experience inadequate return on investment for some of our business initiatives, which would have a negative effect on our operating results.

Growth in our business may not be sustained and may not generate a corresponding improvement in our results of operations.

We may not be able to maintain or improve the levels of growth that we have experienced in the recent past. In addition, although we have recently experienced strong comparable store sales, if our future comparable store sales fail to meet market expectations or decline, the price of our Class A common stock could decline. Various factors affect comparable store sales, including the number, size and location of stores we open, close, remodel or expand in any period, the overall economic and general retail sales environment, consumer preferences and demand, our ability to efficiently source and distribute products, changes in our product offerings, competition, current local and global economic conditions, changes in catalog circulation and the success of marketing programs. These factors may cause our comparable store sales results to be materially lower than recent periods and our expectations, which could harm our results of operations and result in a decline in the price of our Class A common stock.

Although we have recently experienced sales growth as a result of a number of new business initiatives, this sales growth may not continue and the level of our sales could return to prior levels if customer response to our

17

Table of Contents

product offerings is not sustained. Many factors can influence customer response to our product offerings and store formats including responses from our competitors, who may introduce similar products or merchandise formats. In addition, sales levels for particular merchandise or product categories may not continue over time if customer demand levels are not sustained. The level of customer response to new store formats including our full line Design Galleries may vary in different markets and store locations. Similarly, the level of customer response to our new Source Book large catalog format, in which we display a greater percentage of our product assortment, may vary in different markets. In addition, there can be no assurance that we will be able to migrate customer demand successfully when we choose to close a store in a particular location in favor of a full line Design Gallery in the same or an adjacent market location. While our objective is to retain a high percentage of customer demand from store locations that we close, there can be no assurance that we will retain a high percentage of sales from stores closed in the future or that we will continue to retain a high percentage of sales from stores previously closed.

In addition, continued increased activity in our business could result in material changes in our operating costs, including increased merchandise inventory costs and costs for paper and postage associated with the mailing and shipping of catalogs and products. We cannot assure you that we will succeed in offsetting these expenses with increased efficiency or that cost increases associated with our business will not have an adverse effect on our financial results.

If we fail to successfully anticipate consumer preferences and demand, or to manage our inventory commensurate with demand, our results of operations may be adversely affected.

Our success depends in large part on our ability to originate and define home product trends, as well as to anticipate, gauge and react to changing consumer demands in a timely manner. Our products must appeal to a range of consumers whose preferences cannot always be predicted with certainty. We cannot assure you that we will be able to continue to develop products that customers positively respond to or that we will successfully meet consumer demands in the future. Any failure on our part to anticipate, identify or respond effectively to consumer preferences and demand could adversely affect sales of our products. If this occurs, our sales may decline significantly, and we may be required to mark down certain products to sell the resulting excess inventory or to sell such inventory through our outlet stores, either of which could have a material adverse effect on our financial condition and results of operations.

In addition, we must manage our merchandise in stock and inventory levels to track consumer demand. Much of our merchandise requires that we provide vendors with significant ordering lead time, frequently before market factors are known. In addition, the seasonal nature of our products requires us to carry a significant amount of inventory prior to peak selling seasons. If we are not able to anticipate consumer demand for our different product offerings, or successfully manage inventory levels for products that are in demand, we may experience:

| | back orders, order cancellations and lost sales for products that are in high demand for which we did not stock adequate inventory; and |

| | overstock inventory levels for products that have lower consumer demand, requiring us to take markdowns or other steps to sell slower-moving merchandise. |

As a result of these and other factors, we are vulnerable to demand and pricing shifts and to misjudgments in the selection and timing of merchandise purchases.

Our growth strategy and performance depend on our ability to purchase our merchandise in sufficient quantities at competitive prices, including our products that are produced by artisans and specialty vendors, and any disruptions we experience in our ability to obtain our products in a timely fashion or in the quantities required could have a material adverse effect on our business.

We do not own or operate any manufacturing facilities. We instead purchase all of our merchandise from a large number of vendors, many of which are the sole sources for particular products. Our growth strategy includes

18

Table of Contents

expanding the amount of products we sell, and our performance depends on our ability to purchase our merchandise in sufficient quantities at competitive prices. However, many of our key products are produced by artisans, specialty vendors and other vendors that may have limited production capacity. In addition, some of our vendors are small and undercapitalized firms. A number of our vendors, particularly our artisan vendors, may have limited resources, production capacities and operating histories. As a result, the capacity of some of our vendors to meet our supply requirements has been, and may in the future be, constrained at various times and our vendors may be susceptible to production difficulties or other factors that negatively affect the quantity or quality of their production during future periods. A disruption in the ability of our significant vendors to access liquidity could also cause serious disruptions or an overall deterioration of their businesses, which could lead to a significant reduction in their ability to manufacture or ship products to us.

Any difficulties that we experience in our ability to obtain products in sufficient quality and quantity from our vendors could have a material adverse effect on our business. In fiscal 2011, we purchased approximately 84% of our merchandise from vendors that are located abroad. Our ability to obtain desired merchandise in sufficient quantities could be impaired by events that adversely affect our vendors or the locations in which they operate, such as difficulties or problems associated with our vendors operations, business, finances, labor, importation of products, costs, production, insurance and reputation. Failure of vendors to produce adequate quantities of merchandise in a timely manner has resulted in back orders and lower revenue in certain periods of our business operation. While we believe our vendors have the capacity to meet our demand, we cannot assure you that our vendors will be able to produce adequate quantities of merchandise in a timely manner in the future.

We also do not have long-term contracts or other contractual assurances of continued supply, pricing or access to new products with our vendors, and generally we transact business with our vendors on an order-by-order basis. Therefore, any vendor could discontinue selling to us at any time. Any disruptions we experience in our ability to obtain our products in a timely fashion or in the quantities required could have a material adverse effect on our business.

We may not be able to locate and develop relationships with a sufficient number of new vendors, which could lead to product shortages and customer backorders, which could harm our business.

In the event that one or more of our vendors is unable to meet the quantity or quality of our product requirements, we may not be able to develop relationships with new vendors in a manner that is sufficient to supply the shortfall. Even if we do identify such new vendors, we may experience product shortages and customer backorders as we transition our product requirements to incorporate the alternative suppliers. In addition, we cannot assure you that any new vendor with which we do business, particularly any new vendor abroad, would not be subject to the same or similar quality and quantity risks as our existing suppliers.

We do not have exclusive relationships with many of our vendors, and there is a risk that our vendors may sell similar or identical products to our competitors, which could harm our business.

Our arrangements with our vendors are generally not exclusive. As a result, most of our vendors might be able to sell similar or identical products to certain of our competitors, some of whom purchase products in significantly greater volume, or enter into arrangements with suppliers that could impair our ability to sell their products, including by requiring suppliers to enter into exclusive arrangements, which could limit our access to such arrangements or products. Our vendors could also initiate or expand sales of their products through their own stores or through the Internet to the retail market and therefore compete with us directly or sell their products through outlet centers or discount stores, increasing the competitive pricing pressure we face.

We may not have adequate remedies with our vendors for defective merchandise, which could damage our reputation and brand image and harm our business.

If products that we purchase from vendors are damaged or prove to be defective, we may not be able to return products to these vendors and obtain refunds of our purchase price or obtain other indemnification from them. Our vendors limited capacities may result in a vendors inability to replace any defective merchandise in a

19

Table of Contents

timely manner. In addition, our vendors limited capitalization or liquidity may mean that a vendor that has supplied defective merchandise will not be able to refund the purchase price to us or pay us any penalties or damages.